EnCana Land O Sedimentary Basin

* Oil Pool — Oil Pipeline

★ 2005/2006 Drilling Program

Topics Page

Part 1 – Project feasibility assessment on Bongor Basin

1.4.2. Pressure from human rights groups and

Part 2 – Exploration of Bongor Basin (Kubla)

After a series of lectures, computer laboratory sessions and discussions on oil exploration projects, the feasibility studies and the quantitative analysis of the existing project in Doba and Bongor (Chad) are given here as the final report of the course.

In Part 1, we will focus on the investigation results in four aspects: geological, location, engineering and markets, which form a comprehensive feasibility report of oil exploration projects in Chad. The information is primarily obtained from web and ATHENS course materials, however, will be discussed carefully and critically.

In Part 2, on the basis of the geographic information extracted from GIS, the layout of a new pipeline will be designed for the new project in Kubla. Then we will compute the required project input parameters and conduct a quantitative analysis by using the software GeoX. The results will be given in forms of NPV, EMV and decision trees. Finally we will suggest on the possible actions taken by the oil companies and World Bank.

Chad is a landlocked country in north central Africa, lying south of Libya. The country shares 5,968 km of border with Cameroon, the Central African Republic, Libya, Niger, Nigeria, and Sudan. Chad has four climatic zones: it has broad, arid plains in the centre, desert in the north, dry mountains in the northwest and tropical lowlands in the south.

The terrain of Chad in central Africa is dominated by the low-lying Chad Basin (elevation about 250 m / 820 ft), which rises gradually to mountains and plateaus on the north, east, and south.

The only important rivers, the Logone and Chari, are located in the southwest and flow into Lake Chad. The lake doubles in size during the rainy season. Lake Chad was once the second-largest lake in Africa but has shrunk dramatically during the last few decades and is now down to less than 10% of its former size, as a result of world climate change.

The Doba basin of Southern Chad forms an extensive intra-continental rift network, initiated by early Cretaceous extension related to continental break-up and ultimately to the formation of the South Atlantic Ocean. The Doba basin extends along the trend of the Central African Fault Zone, trough southern Chad, central Sudan and into Kenya, known as the Central African Rift Subsystem. These are both extensional and transtensional in origin, containing up to 7,500 m of mainly Lower Cretaceous, continental deposits. Much of Cretaceous rift sediments are concealed below post-rift late Tertiary and Quaternary cover.

In the southern Chad basins, sedimentation during the first rift phase proceeded from Barremian to Albian times with deposition of up to 5000 m of continental alluvial, fluvial and lacustrine clastic sediments. The second rift phase terminates against “Senonian” unconformity, separating deformed Rift Phase I and II sections from a generally flat lying younger section. In the Doba basins strike-slip movements caused major transpressional disruption at this time.

Significant episodes of regional inversion uplift and erosion occurred during the late Cretaceous and early Tertiary. The Adamawa region was uplifted along the line of the Neogene to Quaternary Cameroon volcanic trend, causing the removal of up to 2500 m of Upper Cretaceous and Lower Tertiary section from the region around the western Doba and Bongor basins.

Chad became a net petroleum exporter after the Chad-Cameroon pipeline came into operation in 2003 (financed in part by the World Bank). Industry experts still consider Chad currently under-explored, and future oil discoveries could increase petroleum exports even more.

In 2001, the Chad Cameroon Pipeline Development Project (CCPDP) consortium began test drilling in the Doba basin in Chad. In October 2003, first oil from Doba basin arrived at the port of Kribi. Oil from the CCPDP is produced primarily from three major fields: Bolobo, Komé and Miandoun. The smaller Nya field began producing through the CCPDP infrastructure in 2005, and the Moundouli field will produce through the CCPDP infrastructure once it comes online in early 2007.

Chad

Divestiture Activities Underway

EnCana Land O Sedimentary Basin

* Oil Pool — Oil Pipeline

★ 2005/2006 Drilling Program

Permit H (50% Wl, Operator)

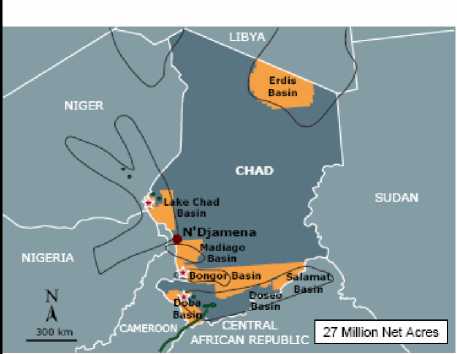

■ 3 oil discoveries in the Bongor basin - Mimosa, Kubla and Baobab.

■ Drilling 3rd well (Karite-1} in a 3-well program in the West Doba Basin.

• Exploration and appraisal drilling will resume in the Bongor basin in November.

■ Divestiture activities underway. BNP Paribas hired to advise on the sale process. Sale is expected to close in the first half of 2007.

EnCana Corporation

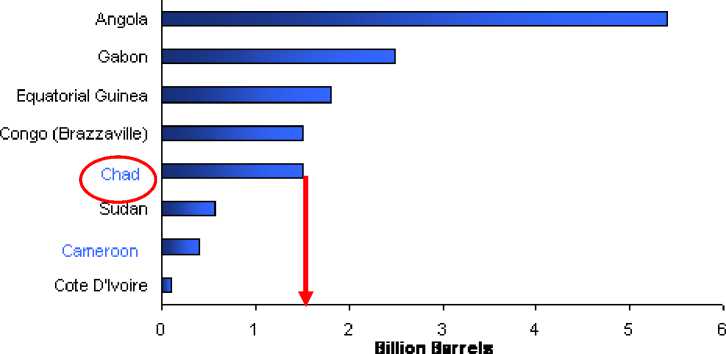

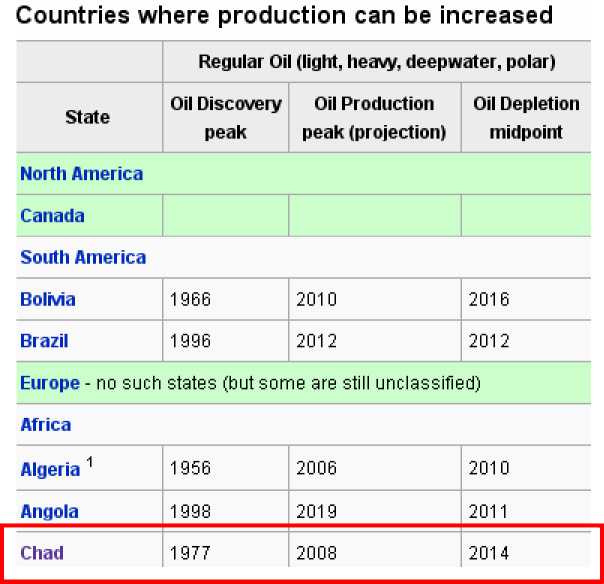

According to Oil and Gas Journal (OGJ), Chad had proven oil reserves of 1.5 billion barrels as of January 2006. International oil companies first discovered oil in the early 1970s in southern Chad in the Doba and Lake Chad basins. However the production does not start until recently (2003), due to the continuous political instability in Chad. The projected peak production will be in 2008 and the oil depletion mid-point will be in 2014 (refer to the following figures for detailed information).

Top Sub-Saharan Africa* Proven Oil Reserve Holders, 2006

Source: Oil and Gas Journal, World Oil

‘Excluding Nigeria (35.8 Billion Barrels) to maintain scale

Proved oil reserves in 2005, (according British Petrol - report 2005)

The total quantity of oil was confirmed, but the oil has been more difficult to extract than expected and daily volumes have thus been lower than anticipated. That is why “High Pressure Water Injection System” was built to push water deep underground into the oil deposits to move oil towards the oil wells and, it is hoped, improve the daily production volume. This new technique will help overcome one of the challenges of Chad’s oil fields discovered only after production began.

The oil industry classifies "crude" by the location of its origin (e.g., "West Texas Intermediate, WTI" or "Brent") and often by its relative weight or viscosity ("light", "intermediate" or "heavy". The price of crude oil exploited in Chad is $10 lower in comparison to Brent in the light of its poorer quality (heavy oil with high sulphur content).

In the south Chad, there is an annual rainy season when floods usually occur and the lake will double in size. These floods could cause damage to both private houses and social infrastructure, and lead to emergent evacuation of residents and a considerable number of casualties and deaths.

In order to solve the flood situation in the Logone River section between Bongor and N'Djamena, a dam was constructed in 1979 between Guirvidig and Pouss, namely the Maga dam, which also act as a reservoir for the SEMRY rice irrigation scheme. A 100 km long dyke was also built along the left bank of the Logone River between Yagoua and Tékélé 1 to 2 meters above the original bank levels. The combined effect of these structures has successfully lessened the severity of annual flood, however, also led to serious ecological degradation of the floodplain and a decline in biodiversity. A reduction of rainfall in the basin was also recorded since the early 70’s.

The following official statistics in 2006 (as of 6 September) somewhat reflected the severity of flooding damage in Doba:

“1,187 houses and 44 walls collapsed, 365 hectares of agricultural land were inundated; many livestock losses were reported; 135 bags of cereals and 30 bags of cement were spoiled by the waters.”

Other environmental hazards in south Chad include periodic droughts and locust plagues.

In the past, over 80% of Chad's population relies on “subsistence farming” and raising livestock for their livings. Cotton and in a lesser measure livestock have, until recently, provided the bulk of Chad's export earnings. However, Chad's primarily agricultural economy is being boosted by the recent major oilfield and pipeline developments and it has been estimated that income from oil increased Chad's per capita GDP by 40% in 2004, and may double it in 2005.

Chad's economy has long been handicapped by its landlocked position, poor internal communications, high energy costs, scarce water resources and a history of political instability. Until now, Chad still relies mainly on foreign assistance and foreign capital for most public and private sector investment projects. However the expected oil income will transform government finances.

Since this project is not only owned by international oil companies, but it is also partly financed by World Bank, a condition of assistance has been insisted on a new law which requires that 80% of oil revenues will be spent on development projects.

However, in January 2006 the World Bank suspended its loan program to Chad, in reaction to the Chadian decision to "relax" laws governing the spending of oil money, which further exacerbated Chad's financial problems. Multiple strikes by government workers, teachers and doctors, were evoked and leading to drastically-shortened school years and a shortage of health care. In an attempt to address the problem, representatives from the World Bank and the Government of Chad later signed a new memorandum of understanding under which the Government of Chad committed 70 percent of its budget spending to priority poverty reduction programs, and provided for long-term growth and opportunity by creating a stabilization fund. The government agreed to enhance transparency and accountability with a new pledge of support for the role of Chad's independent oil revenue oversight authority.

Provided that stability is maintained, the outlook for Chad's economy is expected to be better than it has ever been, although government corruption and continued lack of pay to government-employed functionaries still pose significant obstacles to the country's development.

Some basic economic information about Chad (in US$):

|

GDP (2003) |

$2.65 B |

|

Per capita income |

$237 (2003) $1,519 (2005) (due to oil production) |

|

Natural resources |

Petroleum, natron (sodium carbonate), kaolin, gold, bauxite, tin, tungsten, titanium, iron ore |

|

Agriculture (2001, 38% of GDP) |

Products--cotton, gum arabic, livestock, fish, peanuts, millet, sorghum, rice, sweet potatoes, cassava, dates, manioc. Arable land-- 30% |

|

Industry (2001, 13% of GDP) |

Types—meat-packing, beer brewing, soap, cigarettes, construction materials, natron mining, soft-drink bottling |

|

Services (2001, 49% of GDP) |

---- |

|

Central government budget (2002) |

Revenues--$161 million. Expenditures--$611 million |

|

Defense (2002) |

$31 million |

|

U.S. aid received (2001) |

Economic, food relief--$238 million from all sources, (including $30 million committed by African Development Bank |

Surface transportation in Chad has been difficult. Of the nation’s 40,000-km network of roadways and trails, only about 650 km of main roads near the capital city of N'Djamena were paved. The local transportation in the region of Doba mainly relies on dusty roads, however, which have the conditions highly dependent on weather. Especially during rainy days, roads will be in poor condition and can be dangerous for travel. During the summer rainy season (mid-June to mid-September) many roads even become impassable or are restricted by rain barriers. On the contrary, during the drier season, clouds of dust rising from the roads can reduce visibility substantially.

Poor maintenance is another problem of the road network. Often there are large ruts and potholes on the surface in spite of general road-maintenance obligation. Some projects have been commissioned for preserving the existing condition and capacity of local road-routes in order to meet the new traffic demand spurred by the construction phase of the consortium project.

In rural areas, drivers often have to watch out for livestock crossing the roads, or even large hawks resting on the middle. These natural birds are not afraid of human activities and may sometimes smash onto drivers’ windshields. Hence drivers have to slow down when approaching the hawks, and allowing them sufficient time to fly away. Finally, drivers should be alerted to old transport trucks travelling between cities, which may not necessary have functioning headlights.

The road network in Doba

Travellers on roads in all areas of the country are also subject to the attack by armed bandits.

Electricity is available in the capital of N’Djamena but is subject to frequent outages. Other areas in the country still rely primarily on small diesel-fueled generators or solar cells with fuel imported from Cameroon and Nigeria. The telecommunications infrastructure is limited.

The head of State is the President Colonel Idriss.

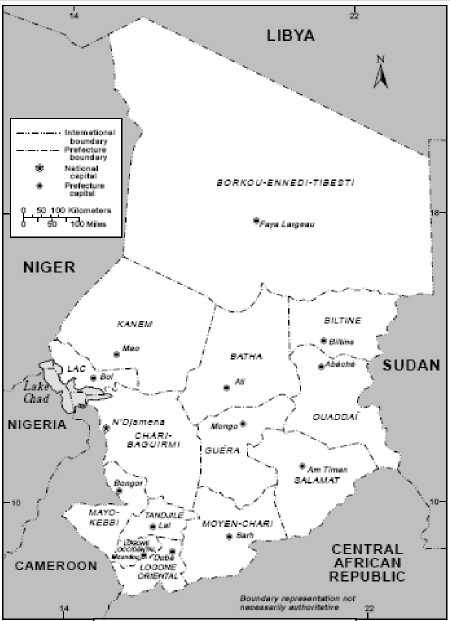

Throughout the 1980s, Chad was divided into fourteen prefectures (refer to the figure on the bottom right). Each was further subdivided into subprefectures, administrative posts, and cantons. Most prefectures were divided into two to five subprefectures; the total number of subprefectures was 54. Administrative posts and cantons were often organized around traditional social units, especially in areas where an existing bureaucratic structure could represent the state. In general, the national government relied on traditional leaders to represent its authority in rural areas. In many of these areas, civil servants could not maintain order, collect taxes, or enforce government edicts without the cooperation of respected local leaders.

Administrators at each of these levels (prefects, sub prefects, administrators, and canton chiefs) were appointed by the president or the minister of interior and remained in office until the president dismissed them. Each prefect was assisted by a consultative council composed of ten or more members nominated by the prefect and approved by the minister of interior. Traditional leaders were often included, and council protocol was sometimes based on local rank and status distinctions.

President Colonel Idriss Deby

14 Prefectures of Chad

During the 1960s, the government granted municipal status to nine towns, based on their ability to finance their own budgets. These municipalities generated most of their revenues through administrative fees, fines, and taxes, and they organized

communal work projects for many city improvements. Their governing bodies were relatively autonomous municipal councils, chosen by popular consensus or informal elections. Each council, in turn, elected a mayor from its own ranks. The official policy of autonomy for municipal councils was generally overridden by the requirement that almost all council decisions be ratified by the prefect or the minister of interior.

The latest political movement was the Fundamental Law of 1982 which declared Chad a secular, indivisible republic, with ultimate power deriving from the people. Both French and Arabic were adopted as official languages, and "Unity-Work-Progress" was adopted as the nation's motto. The constitution authorized the office of president, Council of Ministers (cabinet), National Advisory Council (Conseil National Consultatif--CNC, an interim legislature), and national army. It placed overriding authority for controlling all of these in the office of the president.

The worse internal problem of Chad is its serious corruption. While it is clear that there is little respect for proper procedure, many people believe there is another reason why the oil cash is not getting through. The World Bank agreed to finance this project to help reduce poverty, but the way oil revenues are being managed, this will never happen. It was supposed to be the World Bank's flagship project, a way of eliminating poverty and corruption. But after three years into this project, ordinary Chadians are still waiting for their share of the country's oil riches.

Chad gained independence from French in 1960. However, the first president, Francois Tombalbaye, was nominated by the French of Sara origin and soon accused of favouring the Sara. Chad then went through about 3 decades of violent conflicts and civil wars. The rebels from the north, associated in the National Liberatio Front Frolinat, guided from Algiers by the socialist Abba Siddik, put up a strong resistance.

Finally, multi-party politics were legalized in 1991. Chad's first Presidential elections since independence took place on 2 June 1996 and President Deby won a five year mandate.

However, the second Chadian Civil War began in December 2005. The conflict grew to involve troops from Chad, and rebel groups. These include the United Front for Democratic Change, Janjaweed, and the Alliance of Revolutionary Forces of West Sudan. The conflict has also involved Sudan which allegedly supported the rebels Libya, which is also accused of supporting Darfur rebels, but has mediated the conflict, as well as diplomats from the Republic of the Congo, Nigeria, Central African Republic, Burkina Faso, and the African Union. African Union mediators may soon be replaced by an international force, risking further escalation of the

conflict. Totally 614 Chadian citizens were killed this time by official figures.

On February 8, 2006 the Tripoli Agreement was signed, which brought a cease to the conflict for approximately two months. However, with the recent rebel assault on the Chadian capital, N'Djamena, Chad has broken off all relations with Sudan, effectively nullifying the agreement and has threatened to expel refugees from the Darfur region, in response of the Sudanese rebels, Janjaweed, being backed by their government.

As Chad is still a developing country, this project has to help in improving the basic working condition of workers by financing some of the priority infrastructure, like water, drainage, and economic infrastructure in N’Djamena, Moundou, Sarh, Abéché and Doba. By packaging public works appropriately and using, when possible, laborintensive methods, the project will create employment opportunities for unskilled and semi-skilled labour and promote small and medium enterprises (SMEs) in construction and urban services. An oil exploration project cannot be successful without the contribution by local skillful workers and contractors.

The Chad-Cameroon pipeline had an off-shore oil spill occurred near the town of Kribi in coastal Cameroon and another off the coast of Cameroon occurred later. The slow response time and allegations that the public was not duly informed raised severe criticism from the international societies on the safeguards on coping with a larger accident, especially it is a project co-operated with World Bank. Hence the oil spill response plan, as a part of its obligations as stated in the Environmental Management Plan (EMP), is required by the pipeline project and should be put more focus in order to avoid similar accidents from happening again.

Now a major spill drill mobilized responders and emergency operations centres will deal with a significant hypothetical crude oil spill that would affect coastal area of Cameroon near the marine terminal. The scenario required deployment of trained spill

response teams using equipment such as booms and skimmers from a cache of spill response equipment. The lengths of boom, designed to contain oil floating on water, were deployed at critical locations, as designated in the “Project’s Area Specific Oil Spill Response Plan”. Specially designed inflatable boom was deployed across the surf line. Boom was also strung across the mouth of a river.

A boom designed for doping oil spills

Waste management

The waste management in Doba has been controlled by Esso. At the end of 2006, the project had around 2,700 tonnes of hazardous waste in storage and waiting for processing, nearly all of it is now at the Komé Waste Management Facility. Some of the stored waste is awaiting batch recycling following guidelines set in the EMP. Other material had been held in storage pending the repair of the project’s hazardous waste incinerator system. The incinerator now had been repaired and brought back into service.

Air pollution control

The dust has to be controlled in the outfield areas. An air quality monitoring study, which aimed at the road dust issue, has been extended to make sure all seasonal effects have been taken into account. The first monitoring took place in mid-2006 as the rainy season was arriving in southern Chad. In December, another round of sampling began to assay conditions during the dry season.

Although the project has been flaring 40% to 80% less than other facilities that operate at similar production levels, it has launched a new flare reduction program to further reduce flaring as much as possible.

The project management has two main components:

The Doba Project Management Component (about US$ 20 Million) designed to support the implementation of the Doba project;

The Petroleum Sector Management Component (about US$ 5 million) designed to support the development of Chad's petroleum sector.

They aim at:

• Building environmental, social and technical capacity, both in the Ministry of the Environment (MEWR) and the Ministry of Petroleum (MMEP), starting with the Doba project;

• Mitigating induced impacts on the producing region through the financing of rapid intervention measures such as health facilities and water-wells;

• Supporting development activities in the producing region, including the establishment of a pilot development fund to test financial and implementing mechanisms for complementary rapid intervention measures and mid-term development activities that will be proposed by the community and local NGOs;

• Implementing a communications campaign to limit influx of migrants into the region

• Supporting the development of a management information system (MIS);

• Implementing communication and consultation activities to generate accurate information regarding the project and support information dissemination and dialogue with all stakeholders;

• Building government's capacity to deal with legal, financial and other technical aspects of the Doba project;

• Provide operational support for coordinating project implementation.

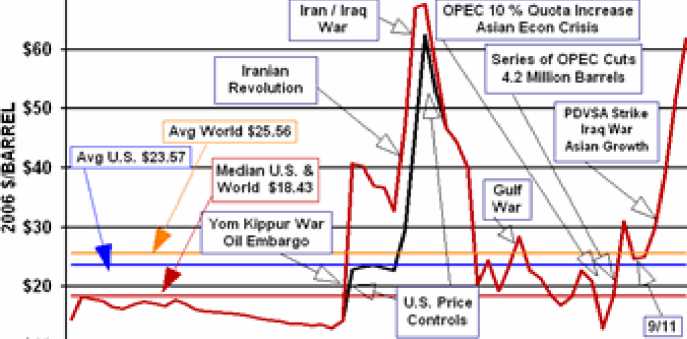

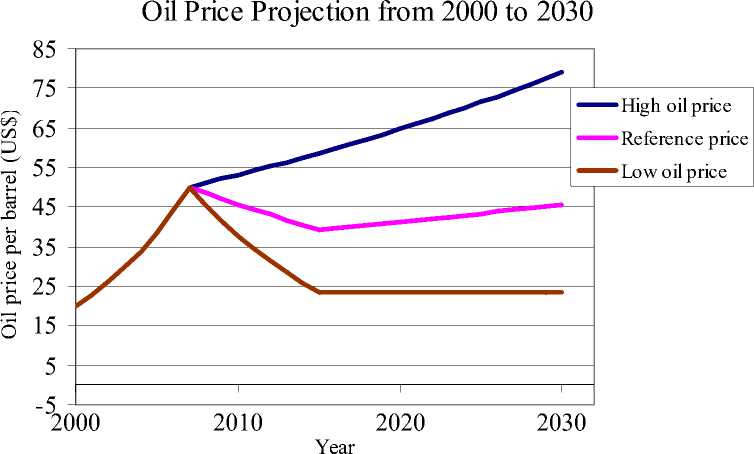

As the main product of oil project is crude oil, the global oil price trend induces significant effect on the profitability of project. Crude oil prices behave much as any other commodity with wide price swings in times of shortage or oversupply. The crude oil price cycle may extend over several years responding to changes in demand as well as OPEC and non-OPEC supply. From the past history (see the past crude oil prices below, in 2006 US$), the supply side was mainly affected by political issues, such as production interruption due to war, conflicts between countries, oil regulation policy by US and, recently, the oil supply reduction policy by OPEC. On the other hand, the demand side was the response to recent economic atmosphere and economic cycle. For example, the economic bloom of US and Asian countries in the 90’s induced an increasing trend in oil price while the East-Asian economic crisis in 1998 led to almost a historical low in oil price. Hence, in order to predict the oil price projection, a detailed research on the future political atmosphere and economic cycles is necessary.

Crude Oil Prices

JflClb Collar*

5/0

$10 -1—--——. iim—i - t i . i.............—r—m—i——

47 49 $1 53 84 ST M 61 KJ 65 CT 69 71 73 75 77 79 81 93 86 87 89 91 93 96 97 99 01 03 OS

48 SO 52 54 56 58 60 62 64 66 68 70 72 74 76 78 83 82 84 86 88 Oj 92 94 96 88 00 02 0406 ‘

1947 - Sept 2006 WTRGfconemfc* 1W8-2006

U.S- 111 Purchase Price | We Une id ) ----"Wortd Price" ■ www.wtr9.caan f479| 293-4091

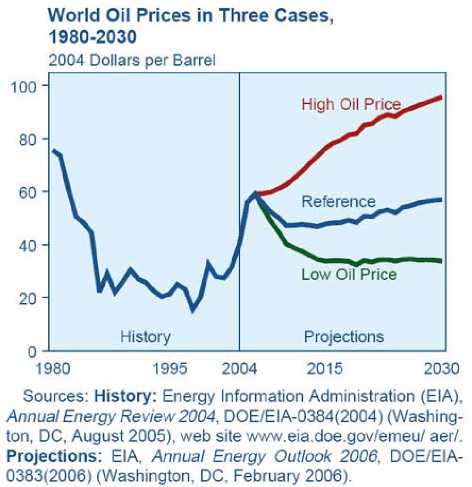

As oil is a non-renewable resource, the recoverable petroleum reserve on Earth and the development progress on renewable energy sources such as solar power and wind power would also affect the future oil price. Nevertheless, the project life in Doba is expected to be around 20-30 years, and if such a severe shortage in oil supply and breakthrough in renewable resource (especially for fuel source for transportation) do not exist in the near future, their effect on oil price becomes negligible.

From the energy statistics from US government (Source: International Energy Outlook 2006 by Energy Information Administration (EIA)), the highlight on the future oil market can be used as a sound reference on the possible projection on oil price until 2030. From their report, the following assumptions on the reference case were adopted:

1. China, India, and the other nations of non-OECD Asia are expected to experience combined economic growth of 5.5 percent per year between 2003 and 2030

2. World oil demand grows from 80 million barrels per day in 2003 to 98 million barrels per day in 2015 and 118 million barrels per day in 2030 (Total increase in 47% from 2003 to 2030 with an average of 1.4% per year), as the world continues to experience strong economic growth.

3. Much of the world’s incremental oil demand is projected for use in the transportation sector, where there are few competitive alternatives to petroleum; however, several of the technologies associated with unconventional liquids (gas-to-liquids, coal-to-liquids, and ethanol and biodiesel produced from energy crops) are expected to meet a growing share of demand for petroleum liquids during the projection period.

1. Increase in oil reserve trend due to technological factors (more oil reserve discovered and increase in recovery rate of discovered oil wells), especially in Iran, Saudi Arabia, Kuwait, Venezuela and Africa

To assess uncertainties in the reference case projections, IEO2006 also includes a high oil price case and a low oil price case. In the former case, worldwide crude oil resources were assumed to be 15 percent smaller, and thus more expensive to produce, than in the reference case, and the preferred production levels of OPEC producers were reduced. In the latter case, the worldwide petroleum resource was assumed to be 15 percent larger and therefore cheaper to produce than in the reference case, and OPEC preferred production levels were increased. In all the cases, world oil prices are expressed as the average price of imported low-sulphur, light crude oil to U.S. refiners (Hence a deduction in value of US$10 per barrel is adopted for Doba basin due to its heavy oil content).

Due to the large possible fluctuation in oil price, all the three cases (high oil price, reference and low oil price) will be inputted into modelling in Part 2 for comparison.

As an oil company established in the western society, corporate social responsibility (CSR) have always been closely monitored by human rights groups and reported to shareholders. More importantly, this Exxon-mobil project has been in co-operation with World Bank and aims also at improving the poverty situation and human rights in Chad. Any violation to human rights would be sensitive to severe criticism by the mass media and pressure groups which in turn affect the confidence of shareholders in further investment and good-will of the company.

A similar controversial oil exploration project in South Sudan (just next to Chad) can be referred as a sound example. Renowned organizations, such as the British Christian Aid, have documented oil-related human rights abuses, such as a systematic government policy of depopulating oil-rich areas. Unavoidably, oil companies have also been accused of nurturing human rights abuses. New lines of armed conflict were created from the governmental capital raised from oil revenue. As a result of the great pressure, the western oil companies have to gradually withdraw from the area even the investment has not been recovered. For example, shareholders of Talisman were continuously expressing concern on the issues about Sudan and its shares were continuously being discounted based on perceived political risk in-country and in North America. Then, in September 2006, the Austrian government-controlled oil company OMV also sold its exploration blocks after a massive campaign by human

rights groups. Even Swedish Lundin Petroleum AB also offers the remaining shares for sale at present.

Moreover, political instability may also force the oil companies pulling out of the region immediately and lead to loss in initial investment. A recent example may include the Chevron’s pulling out in 1983 due to Sudanese civil war and declining security conditions in the oilfield area.

In order to assess the risk in Chad, the political and economic stability between Chad and Sudan can be compared. From “Political and Economic Risk 2007” for Chad and Sudan, the potential risk of investment in both short term and long term were assessed:

|

Export transactions |

Direct investment | ||||||

|

Political risk Short Medium/ term Long Term |

Special transact-tion |

Commercial risk |

War risk |

Risk of expropriation and Gov. action |

Transfer risk | ||

|

Chad |

4 |

7 |

5 |

C |

6 |

N.A. |

6 |

|

Sudan |

6 |

7 |

6 |

C |

6 |

5 |

7 |

It can be observed that the oil exploration project in Chad is quite comparable to that in Sudan and there also exists high risk in the aspects of civil war, political instability and, additionally, the possibility of pulling out due to human rights pressure from the international society. Any sensitive news in the area could affect the confidence of investors of the company and finally the negative effect will be reflected in the discount of share prices, just like what Talisman has been confronting a few years ago. Hence a high discount rate and required IRR will be used for modelling.

It is expected that the Asian economies, especially those of India and China, will continue to grow rapidly in the near future. As a development strategy in the past two decades, Asian national oil companies (NOCs) have been aggressively exploring for and producing oil in Africa so as to ensure a stable supply for fulfilling their substantial energy demand. Their recent expansion mainly relies on taking over the oil wells pioneered by international oil companies (IOCs) as they can develop the projects without the burden of concerning issues like development of fundamental human rights, transparency in governance and accountability in oil revenues reaching the citizens. They are now still “thirsty” for more oil supply and will try all possible ways to purchase more oil interest in Africa as a diversified oil supply. For example, after the Chinese oil company CNPC entered Sudan in 1996, they are also interested in taking over some of the oil exploration interest in southern Chad and diverting it eastwards to its Sudan pipelines. However this would also affect the current oil project related interest enjoyed by Cameroon and lead to another new round of

political and commercial disputes.

As a result, it can be seen that this Chad project has quite a large market value due to huge oil demand both in the western society and Asian development. The more and more tightened oil supply expected will further attract its investment interest from oil companies all around the world.

Apart from rapid economic growth in the U.S. and some Asian countries, the recent high oil price is also caused by the collaboration of OPEC’s supply reduction. The oil price has the OPEC floor of $50 a barrel and now stabilized at $60. Since the OPEC countries own most of the oil reserves in the world (they are mainly from Middle-East and some of the African countries), their current pricing strategy will continue to ensure a high oil market price in the future.

After the extensive information research on Chad, the core aspects of the project, geological description, location investigation, engineering issues and markets, are explained. Both the possible risks and potential benefits are taken into consideration.

The highlight of risks includes possible oil spillage due to annual floods, low skills of local labour and contractors, poor transportation and communication infrastructure and, political instability and most importantly, the low transparency and corruption problem of Chadian government. All these factors may further increase the uncertainty and cost of project. If the last resort, immediate pulling out of Chad, has to be taken due to emergent incident such as eruption of civil wars, the loss can be substantial and even affect the foundation of the oil companies and World Bank.

However, this is also a prospective project. From the pricing strategy of OPEC on oil and expectation of strong economic growth in the world, it is forecasted that the oil price will continue to stay in a relatively high level at least in next three decades. The potential revenue generated is high. This does not only add on the profitability of oil companies, but also provide an unprecedented development opportunity for the landlocked Chad. Since the oil fields start their operations, the GDP of Chad has also been increased substantially. With the involvement of World Bank loans to Chad, political pressure can be exerted on the local government on the issues such as improving the current severe corruption situation, protecting basic human rights and commencing necessary infrastructural projects.

In the technical point of view, the layout of new pipelines should avoid the annual flood areas and local agricultural areas, if possible, so as to minimize the threat of oil spillage. The engineering management systems should be well introduced to all the team members and the Environmental Management Plan (EMP) should be prepared for continuous monitoring and actions to be taken if accidents happen. To let the local society enjoy the development opportunity, more training should be provided to local labour and contractors so that they can participate in the project actively.

In conclusion, the project is still a feasible one and will be successful, however, only with the close monitoring on political issues in Chad and the collaboration of World Bank. A high required internal rate of return (IRR) and discount rate have to be assumed for the quantitative analysis so as to balance the potential risk.

In the second part of this report, two computer programs were used: DIVA-GIS and GeoX

DIVA-GIS

It is a database for integrating and analysing geographic information. Various layers of information have been inputted already, such as local crops distribution, annual flood areas, locations of refugee camps, oil exploration areas, etc. By selecting the required ones, the layout of new pipeline can be planned more easily. One point to note is the data consistency, which has to be checked all the time. In the occasion of discrepancy, one has to decide which piece of geographical information to be more creditable.

GeoX

It is a software for evaluating perspective, risks and economic prospect of the oil project. It is divided into two parts - technical analysis and economic analysis. For a technical analysis, the main data required include volumetric parameter estimates used to estimate in-place resources and recovery rate estimates used to estimate recoverable resources. For an economic analysis, we need exploration, development and production activity level, unit capital expenditure and operating cost estimates, petroleum price scenario and fiscal regime parameters. The prospect analysis is also given which is used to determine both how attractive the oil field is in terms of oil and gas potential and what the risks are that oil field might turn out to be non-economic.

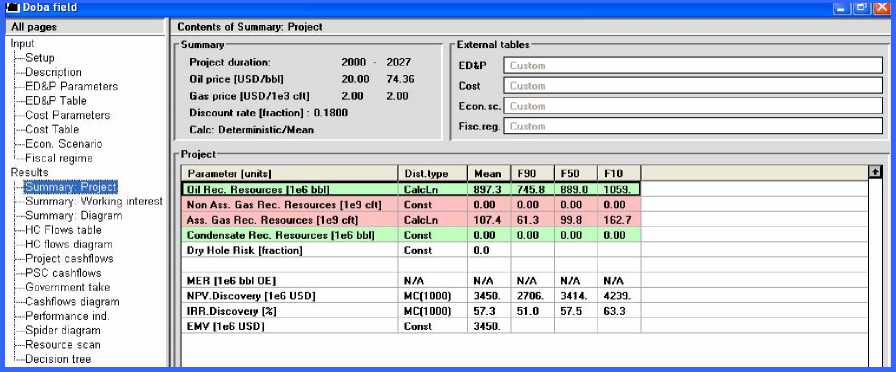

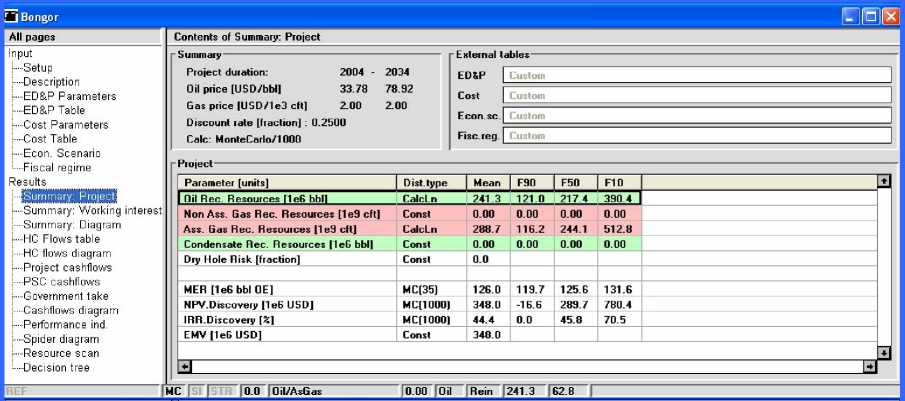

Since most of the parameters for Doba have been given already (except economic scenario analysis of oil price), only the Kubla parameter input will be discussed here.

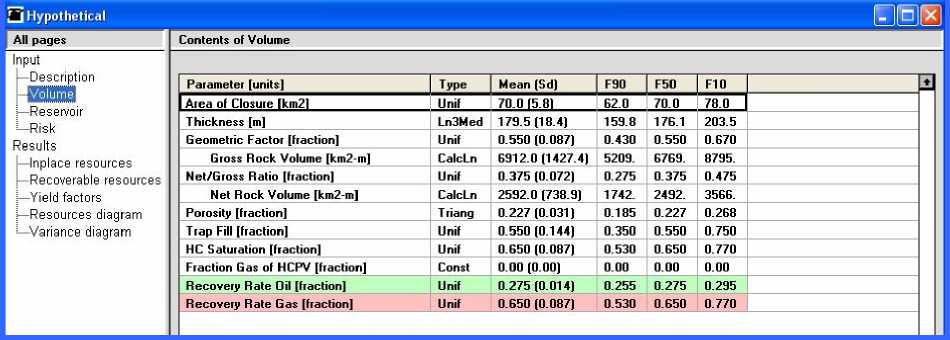

Due to insufficient information on the exact volume of the oil reserve in Kubla, we have to estimate it from the other known oil field data in the region. By multiplying the regional average oil thickness of 176.1 m and our site area of 70km2, the oil reserve is estimated at around 877.5 MMbbl.

A new pipeline has to be constructed for connecting the new Kubla oil field and Doba where the existing Chad-Cameroon pipeline starts. With the references from part 1 about Chad, the following aspects have been taken into account for the layout of the new pipeline:

|

Aspect |

Description and consequences |

|

Geographical barriers |

Rivers, roads, bridges and major cities. Should be avoided, if possible, but will lead to increase in total pipeline length and cost. |

|

Flooding areas |

Areas where annual floods are likely to occur. Higher per length construction cost and higher risk in oil spillage. |

|

Refugee areas and camps |

Location where refugees from other African countries are settled temperately. May affect the reputation of project if a large area of them has to be relocated. |

|

Agricultural zones |

For growing corps like rice, peanuts and cotton. Extra cost for land compensation. Local farmers may lose the only way of sustaining their livings even after land compensation. Catastrophic consequence of oil spillage leading to further shortage of food. |

|

Protected areas |

Areas with environmental interest |

All these aspects are considered in balance with the oil company’s benefit (of minimizing the cost) and the Chadian interest, as the approbation of the Chadian government and co-operation of local residents are necessary for new constructions. Sometimes even the agreement by NGO’s like “Green Peace” is also important due to their considerable influence on local people, which will subsequently affect the reputation of the project. Hence an economical, safe and ecological pipeline is our ultimate goal.

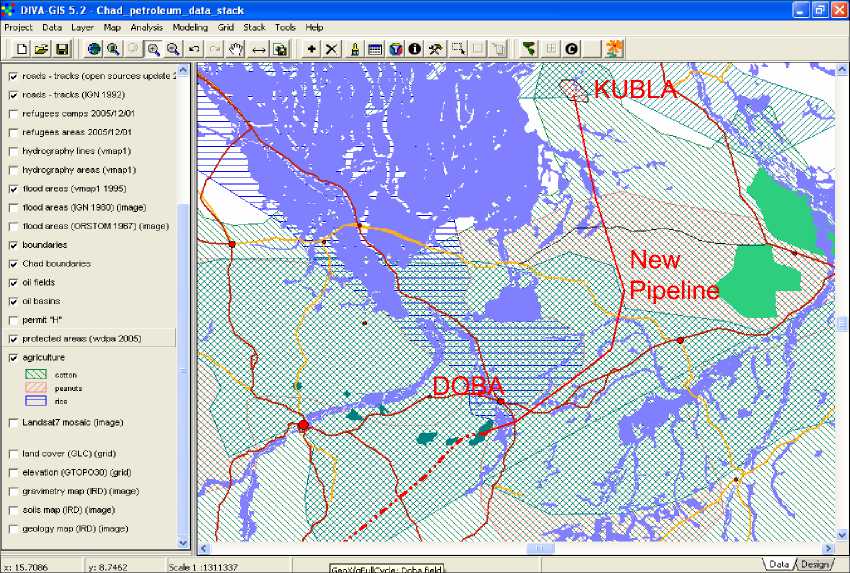

From the GIS, neither protected areas nor protected areas are found near Kubla. For the agricultural zones, the rice growing areas are avoided in light of the importance of food. However, a large piece of cotton growing areas exist between Kubla and Doba which are unavoidable unless a very indirect route is chosen. We choose to by-pass it as cotton growing has become less important in Chad (due to continuous decrease in cotton price in the recent years). Lastly, the layout is set near to the main road for quick access such that emergent maintenance reaction is convenient in case of any possible breakdowns of the pipeline. Here is final layout of the new pipeline:

From the chosen layout, the length of new pipeline is estimated at 190km, on land and approximately one-third lying near to flood areas. By the cost estimation table developed from many oil pipeline projects in the world, the cost of sections near to flood areas will be approximately 50% higher (see below).

|

Pipeline situation |

Construction cost per length (in US$) | |

|

In the sea |

180.000 $/km | |

|

In dry land |

90.000 $/km |

◄----- |

|

In flood plains or wet lands |

140.000 $/km |

◄----- |

|

Completely raised on piles |

250.000 $/km | |

As mentioned before, there are also many other items in addition to construction cost such as land compensation and the actual cost of construction may also deviate from geographic positions. Hence instead of a detailed breakdown of cost, the total length and total cost of Chad-Cameroon pipeline was referred, which is a good reference of similar pipeline projects in Africa. The total cost per length (including land compensation, extra cost, etc) in dry land is about $1.4M/km. The fixed development cost is calculated by the area ratio between regions with a reduction factor (because there are some existing infrastructural developments already).

Summary of some parameter inputs to GeoX:

|

Accumulation size |

877.5 |

(Mbbl) |

|

New Pipeline |

190 |

(km) |

|

Area of closure |

70 |

(km2) |

|

Thickness |

176.1 |

(m) |

|

Cost per km |

1.4 |

(US$M) |

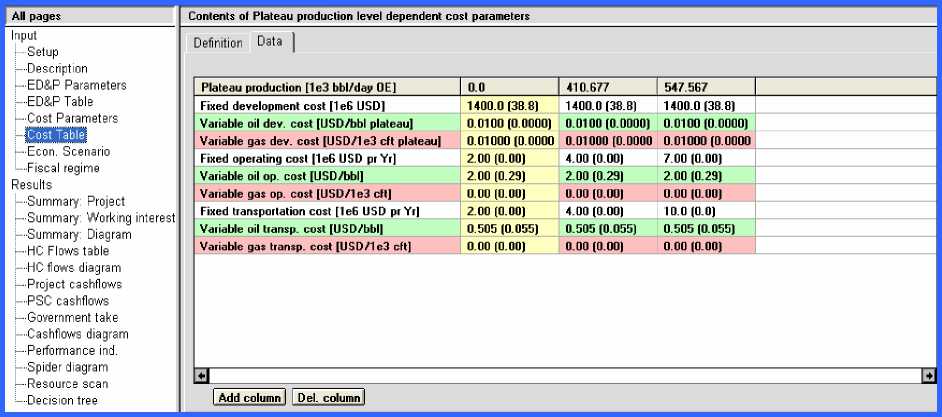

Calculation of total project cost in Kubla (Cost Table):

US$ M

|

Fixed Development |

1100 |

|

New Pipeline |

266 |

|

Total |

1366 |

|

Round-off input |

1400 |

Since the geological features of two projects are quite similar, other geological parameters are assumed to be in agreement with those adopted for Doba basin.

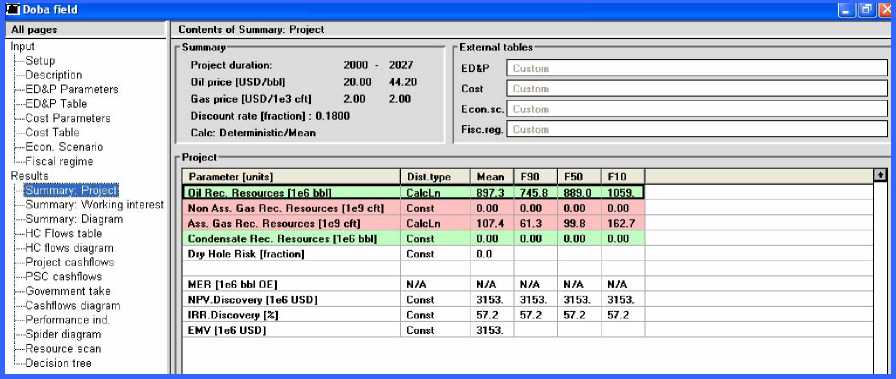

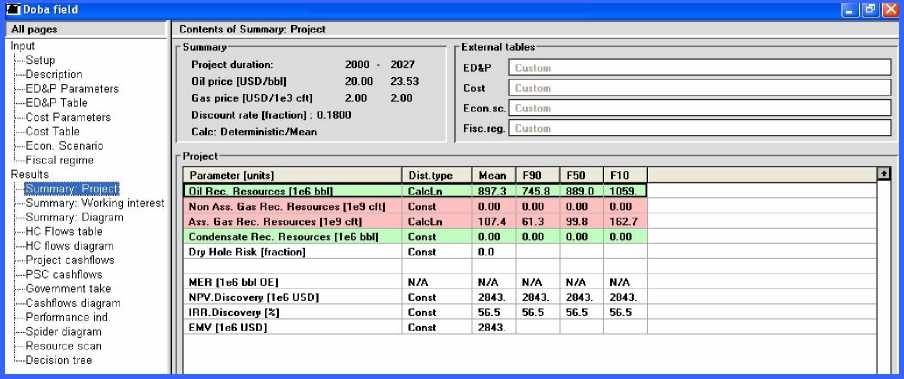

From the markets analysis in Part I, the oil price projection from 2000 to 2030 can be assumed in three cases: High oil price, reference price and low oil price. Here are the parameters adopted for the program input:

|

Oil Price |

High oil price |

Reference price |

Low oil price | |||

|

USD per barrel |

Change per year |

USD per barrel |

Change per year |

USD per barrel |

Change per year | |

|

2000 |

20 |

14% |

20 |

14% |

20 |

14% |

|

2007 |

- |

2% |

- |

-3% |

- |

-9% |

|

2015 |

- |

1% |

0% | |||

|

2030 |

- |

- |

- |

- |

- |

- |

“Print-screen” of parameter input in GeoX (for Kubla):

Cost table

Hypothetical volume input:

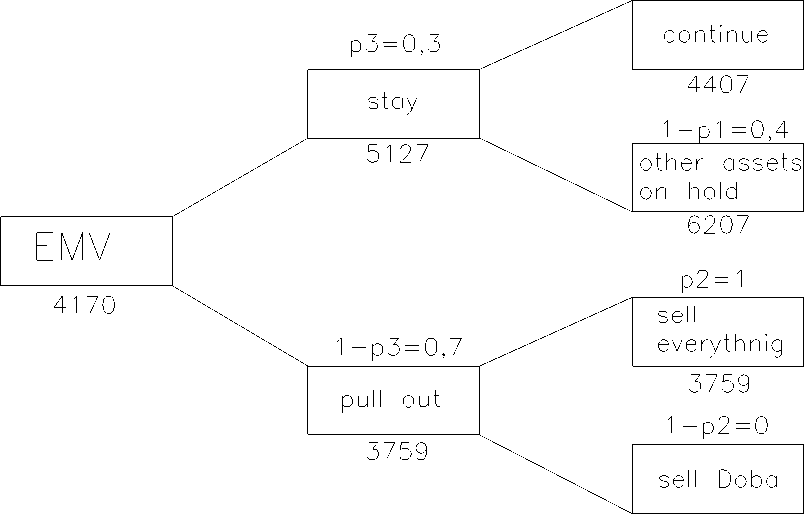

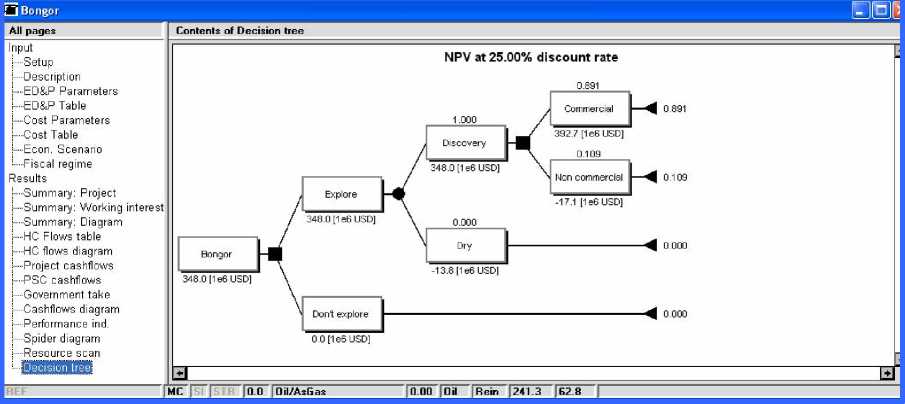

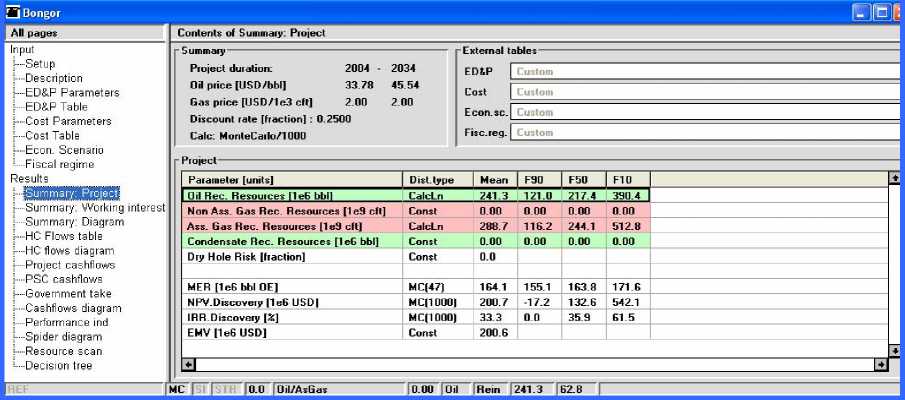

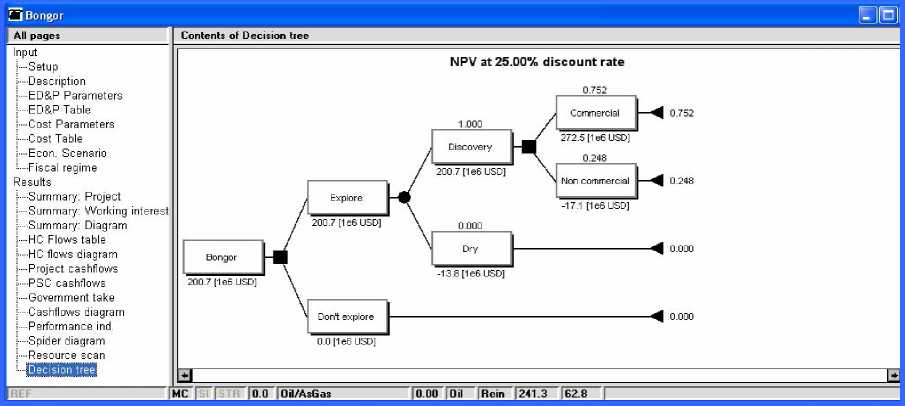

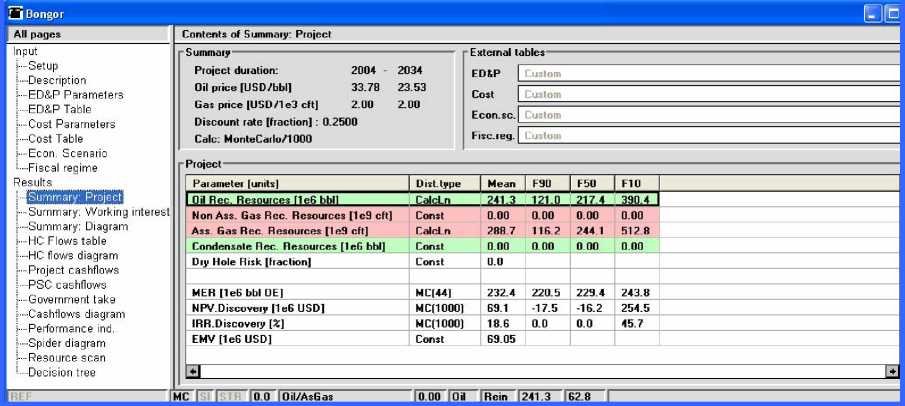

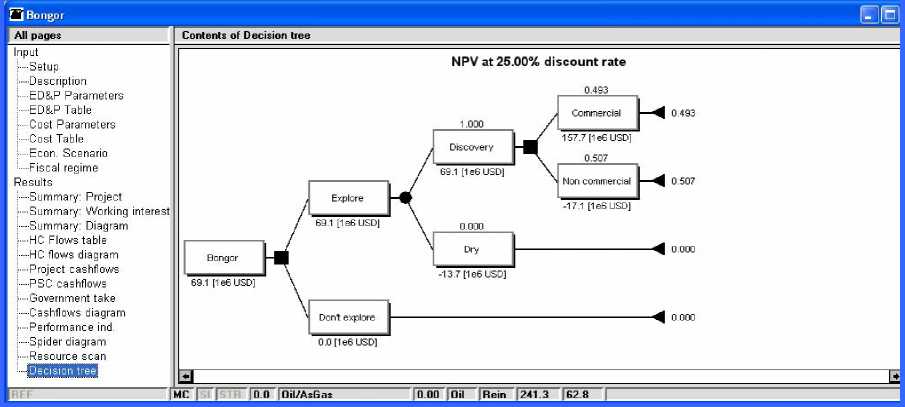

In order to draw decision trees for the Chad project evaluation, the following parameters have to be evaluated:

From the result “Project Cash-flow” of GeoX, the “net cashflow after tax” was calculated for each year. The project net present value (NPV) can be calculated by the summation of their discounted values (in 2007 figures), i.e.

NPV =

N z n =1

R - d (1 + r))

As conducting an oil project in a developing country like Chad is a high-risk and long-term business, discount often has to be given in order to attract new international buyers. On the other hand, with the success in Doba exploration since 2003 and large amount of known project parameters such as recovery ratio, geological features and estimated reserves, the required discount rate for sale can be smaller, i.e. 40% (or a factor of 0.6) is assumed.

Bongor is a relatively new project with its commencement in 2005. The level of risk, incurred by the large amount of uncertainties in exploration, is expected to be higher. Hence a larger discount rate will be given, i.e. 60% (or a factor of 0.4) is assumed.

If staying in Chad,

Since quite a large number of locations in Bongor Basin have been found with oil reserves, the Bongor project is expected to be in good value and high in profitability. Hence if the condition of staying in Chad is given, it is more probable of continuing all the projects than only the Doba one. P1 is assumed to be 0.6. On the contrary, the conditional probability of “only continuing Doba project while keeping other assets on hold”, (1-P1), is assumed to be 0.4.

As introduced in Part 1, this project is in co-operation with World Bank and with most of the governmental oil revenue will be spent on the local Chadians. However, severe local corruption problem has already attracted mass media’s continuous reports and many criticisms have been in doubt of the possibility of fulfilling this commitment. Referring to the example of Talisman’s share drops due to oil project in Sudan, a loss in company reputation is to be taken into consideration here and as large as 30% of NPV will be discounted in staying in Chad.

Since the oil reserves in Bongor (Kubla) oilfields have been confirmed and estimated, any future exploration is possible now and a positive market value is available for sale. Hence P2 is assumed to be 1, while the conditional probability of “only selling Doba”, (1-P2), is assumed to be 0.

The recent criticism on Chad project has quite a lot of similarities of Sudanese project, which was also initiated by a group of IOC’s. Referring to the reality of Talisman and OMV’s actual pulling out of Sudan, the probability of ExxonMobil’s staying in Chad is also getting smaller. Hence P3 is assumed to be 0.3, while the probability of “pulling out of Chad”, (1-P3), is assumed to be 0.7.

NPV of both oil fields (Doba and Kubla) in three possible oil prices scenarios are evaluated from the GeoX result of annual cash-flow and by using the formula introduced in the previous part.

The table below summarizes the NPV’s calculated for each decision and the estimated monetary value (EMV) of whole project, in accordance with the assumptions introduced.

|

p |

High Oil Price |

Reference Price |

Low Oil Price | |

|

NPVDoba |

8221 |

7296 |

6207 | |

|

NPVKubla |

1208 |

420 |

88 | |

|

NPVcontinue both |

60% |

6600 |

5401 |

4407 |

|

NPVcontinue Doba |

40% |

8221 |

7296 |

6207 |

|

NPVstay |

30% |

7249 |

6159 |

5127 |

|

NPVsell both |

100% |

5416 |

4546 |

3759 |

|

NPVsell Doba |

0% |

4933 |

4378 |

3724 |

|

NPVpull out |

70% |

5416 |

4546 |

3759 |

|

EMV |

5966 |

5030 |

4170 |

Note: 1. All prices are in US$M.

2. Formulae for calculations:

NPVcontinue both = NPVDoba + NPVKubla – “loss of reputation”

NPVcontinue Doba= NPVDoba

NPVstay = p1*NPV continue both + (1-p1)*NPVcontinue Doba

NPVsell both = NPVDoba + NPVKubla – discount

NPVsell Doba = NPVDoba – discount

NPVpull out = p2*NPVsell both+ (1-p2)*NPVsell Doba

EMV = p3*NPVstay + (1-p3)*NPVpull out

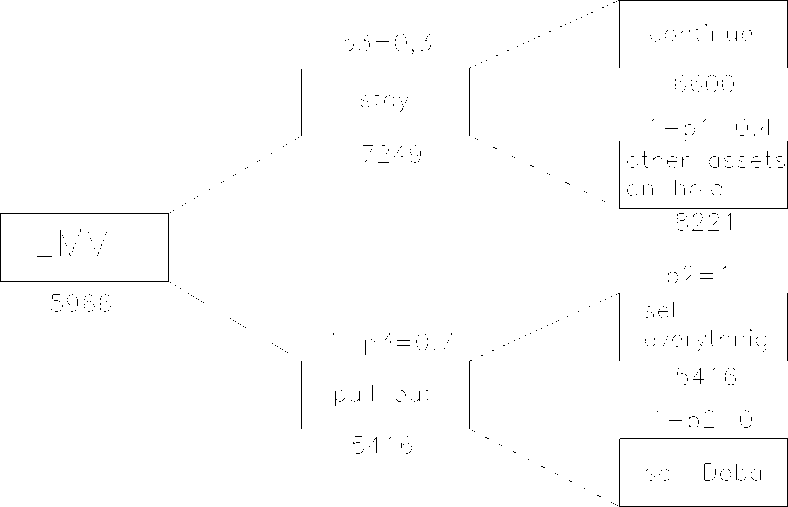

Decision tree for HIGH OIL PRICE

p3 = 0,3

continue

p1 =0,6

stay

5401

5030

6159

1 — p 1 =0,4 other assets on hold

7296

1 -p3 = 0,7

pull out

p2=1

sei everyth nig

4546

4546

sell Doha

1-p2=0

4378

Decision tree for LOW OIL PRICE

Decision trees show that the most valuable decision is “to stay in Chad but continue only Doba” due to high loss of reputation if continuing both oil fields. The loss of reputation is too large in comparison with NPV of Kubla oil field, which is estimated at 40% probability. This conclusion is valid for all oil price scenarios.

The threshold probability (pthreshold) that turns EMV to zero does not exist because both decisions staying or pulling out are positive.

“Printscreen” of other results given by GeoX (for both Doba and Kubla):

Doba (High\oil price)

Doba (Reference price)

Doba (Low oil price)

Kubla (High oil price)

Kubla (Reference price)

Kubla (Low oil price)

After the collaborative research and analysis of our team, the ExxonMobil project in Chad has been investigated comprehensively. In Part 1, the geographic, political and economics conditions in Chad were described, with the information obtained from the informative web resources but also criticized carefully. The feasibility of such an oil project was evaluated by discussing its advantages, disadvantages and potential risks. In Part 2, the required geographic information was extracted from the given GIS and the layout of a new pipeline, in the consideration of the factors explained in Part 1, was designed. The GeoX input parameters were evaluated and the results such as decision trees, NPV, EMV, etc, were obtained. It was concluded that both NPVstay and NPVpull out are positive, probably because of the high IRR incurred by the continuous high oil price level. The EMV of the project has a range of US$ 4,170 – 5,966 M, depending on the oil price projection in the future. No threshold probability was calculated in the light of positive NPV for both cases.

This project shows a good example of investing in a developing country: with high potential high returns and, at the same time, with high potential risk if not handled carefully. This is also the case even for other sectors like banking, manufacturing, trading that their businesses in developing countries can be the fastest growing ones while they also bring the most fluctuating factors to companies. This explains the reason why many IOC’s have initiated their oil explorations in Africa as early as three decades ago despite the political instability.

To achieve a successful project in Chad, the oil companies are recommended to take the following actions simultaneously:

1. Monitor the oil price closely. High potential return is the result of high oil price level. If the oil price drops, consider pulling out of the project if the incurred risk does not drop simultaneously.

2. Continue the co-operation with World Bank, who can exert political pressure on Chadian government for developing the country on both economic and politic sides, which in turn lowering the risk of the project.

3. Offer required oil exploration skills to local people and contractors, who can be one of the active project participators.

4. Communicate with local NGO’s, who can have great influence on governmental bodies and people.

5. Ensure good engineering management and control. Avoid accidents as they can be a source of severe mass media criticism.

6. Co-operate with other NOC’s, if possible who have great desire for more oil explorations and strong foundations for long-term involvement.

Apart from the potential profit to the oil companies, we also hope that this project will also provide a development opportunity to Chadians by improving the human rights situation, openness of government, corruption problem, etc. and finally achieve a winwin situation for all the players.

1. General information on Chad, http://en.wikipedia.org/wiki/Chad

2. Estimated oil reserves in the world,

http://cs.wikipedia.org/wiki/Soubor:Oil_reserves_2005.jpg, http://en.wikipedia.org/wiki/Oil_reserves

3. Athens Course Materials, Richard Sinding-Larsen

4. “Information of Chad-Cameroon project”, Country Analysis Briefs, Energy Information Administration (EIA), http://www.eia.doe.gov/emeu/cabs/Chad_Cameroon/pdf.pdf

5. “Frontier & International New Ventures”, J.K.Brannan, Managing director of Encana, http://encana.com/wcm/groups/internet/@p_www-ir/documents/web_content/p003320.pdf

6. “Chad Export Project Report ”, Esso Exploration and Production Chad Inc., http://www.essochad.com/Chad-English/PA/Files/21_allchapters.pdf

7. “Request for inspection”; “Hydrology and water management in the humid

tropics”, World Bank, http://web.worldbank.org/

8. “World Bank's "model" project in Chad beset by persistent problems”, http://www.bicusa.org/

9. “Present situation of Chad´s water development and management, Chapter 1”,

UNESCO, http://www.unesco.org/

10. “Oil Price History and Analysis”, WTRG Economics, http://www.wtrg.com/prices.htm

11. “International Energy Outlook 2006: Chapter 3: World Oil Markets”, Energy Information Administration (EIA), http://www.eia.doe.gov/oiaf/ieo/oil.html

12. “Talisman Marks End of Era with Completion of Sudan Sale”, Anonymous, Oil & Gas Journal; Apr 7, 2003; 101, 14; ABI/INFORM Global pg. 36

13. “Human Rights Groups Chase Oil Company from Sudan”, Afrol News, 20 March 2007

14. “Political and Economic Risk 2007”, http://www.ondd.be

15. “Asian oils in Africa: A challenge to the international community”, Florence

C. Fee, 24-04-06, http://www.gasandoil.com/goc/company/cna61856.htm

16. “OPEC emerges successful in price strategy”, Syed Rashid Husain, 8-4-2007, http://www.dawn.com/2007/04/08/ebr5.htm

17. “OPEC strategy seeks to maintain $60 barrel price”, Middle-East Finance and Economy, 30-12-2006, http://www.ameinfo.com/106734.html

- 38 -

{kind=link}